How LPL Research Thinks About Dividends

Last Edited by: LPL Research

Last Updated: March 02, 2026

Dividend strategies, a.k.a. equity income strategies, have outperformed to start the year, owing to the value-led cyclical rotation we are seeing in domestic equity markets. Looking beyond current performance, this week, we ask and answer the question “How should I think about dividend stocks or building an equity income portfolio?”

Executive Summary

The idea of lying on the beach while your money works for you is often idealized in the financial media and by financial professionals alike. And why not? Investors love passive income, whether it comes from interest payments via fixed income securities, rental income from a real estate investment, or dividends from a stock portfolio. Our focus is on dividends, and understanding different approaches investors can incorporate into equity allocations. In this week’s Weekly Market Commentary, we analyze different equity income strategies, explain why we believe incorporating quality makes sense, and review technical charts to understand what’s potentially on the horizon for the near-term performance of different equity income strategies.

Key Takeaways

- Look Beyond Simple Dividend Yields. Our research shows that building a systematic dividend income strategy based solely on high dividend yields underperforms strategies based on total shareholder yield (dividend + buyback yield) or dividend growth.

- Pay Attention to Price-Based Returns. When analyzing equity income strategies, it is important to consider both sources of total return: current income and price-based returns (i.e., capital appreciation). Myopically focusing on total return ignores many real-world considerations like taxes, transaction costs, and current income requirements.

- Keep Quality Front of Mind. Given the susceptibility of high-dividend strategies to unknowingly fall into value- or yield-traps, we suggest “paying up” (i.e., accepting a slightly lower yield) to increase quality in any equity income portfolio, but especially in one focused solely on high dividend yields.

- What’s Working Today? Dividend-oriented equities remain in strong uptrends, supported by solid momentum and improving relative strength versus the broader market. The simple dividend yield strategy is currently leading on a short term basis, but longer-term relative trends favor continued outperformance from dividend growth and shareholder yield within the dividend stock landscape.

Equity Income: More Than Just Dividend Yields

For many investors, the desire for yield is a bedrock of their portfolio construction strategy. In this pursuit, dividend-paying stocks are often chosen for a portfolio’s equity allocation, providing a tangible cash return alongside the potential for capital appreciation. The starting point for most investors when building a portfolio of dividend paying stocks is the dividend yield. It is a straightforward, easily calculated figure that provides a framework for stock selection. Simply choose among the highest dividend yields to generate the highest level of income relative to capital invested. This dividend yield approach serves as a baseline strategy for comparison.

We propose an alternative framework for building or selecting an equity income portfolio, built around two enhanced strategies. The first is dividend growth, which shifts the focus from the level of the dividend today to the durability and consistent growth of the dividend over time. The second is shareholder yield, a more comprehensive metric that captures the total capital returned to shareholders by combining dividends with net share buybacks.

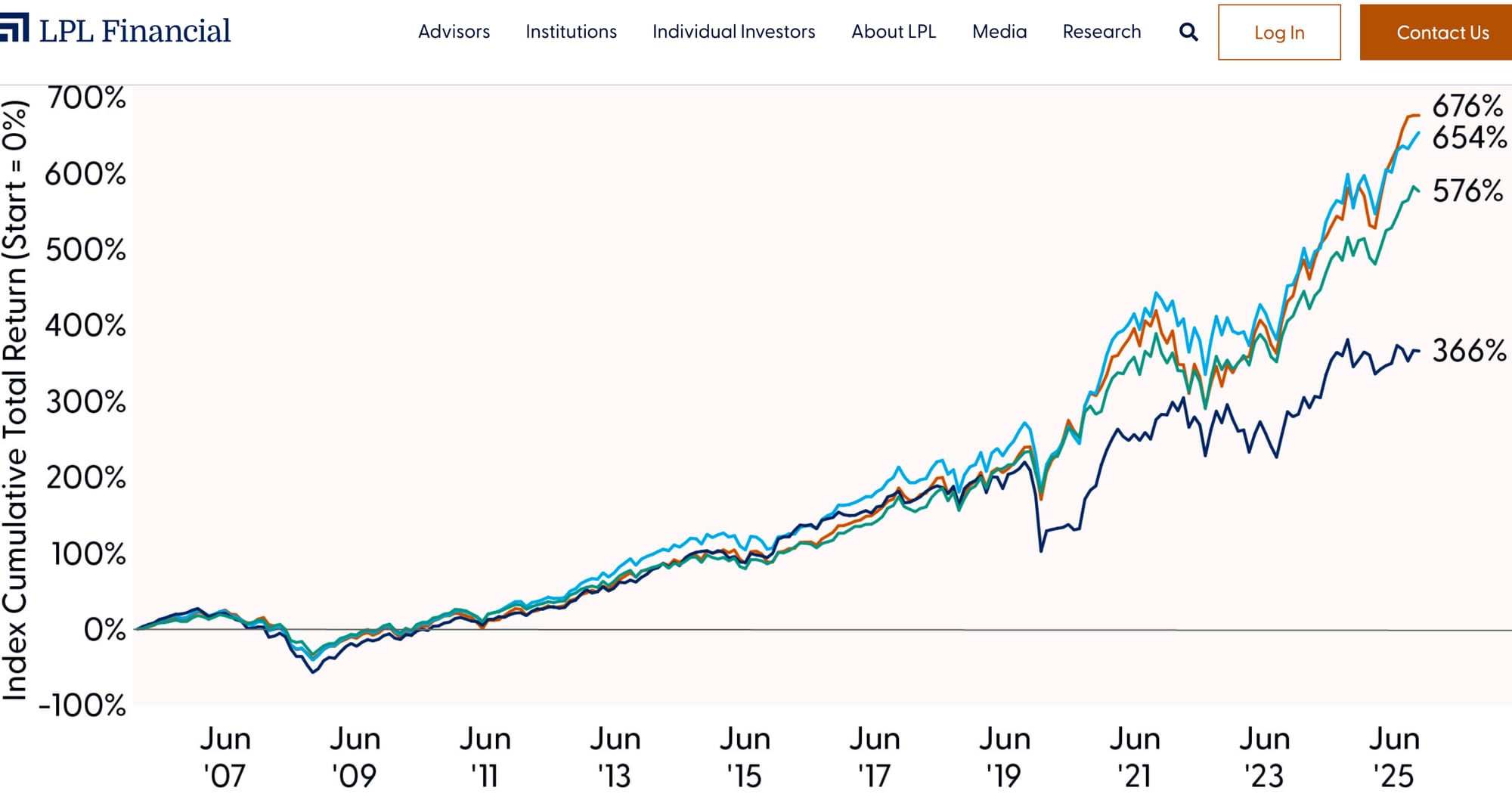

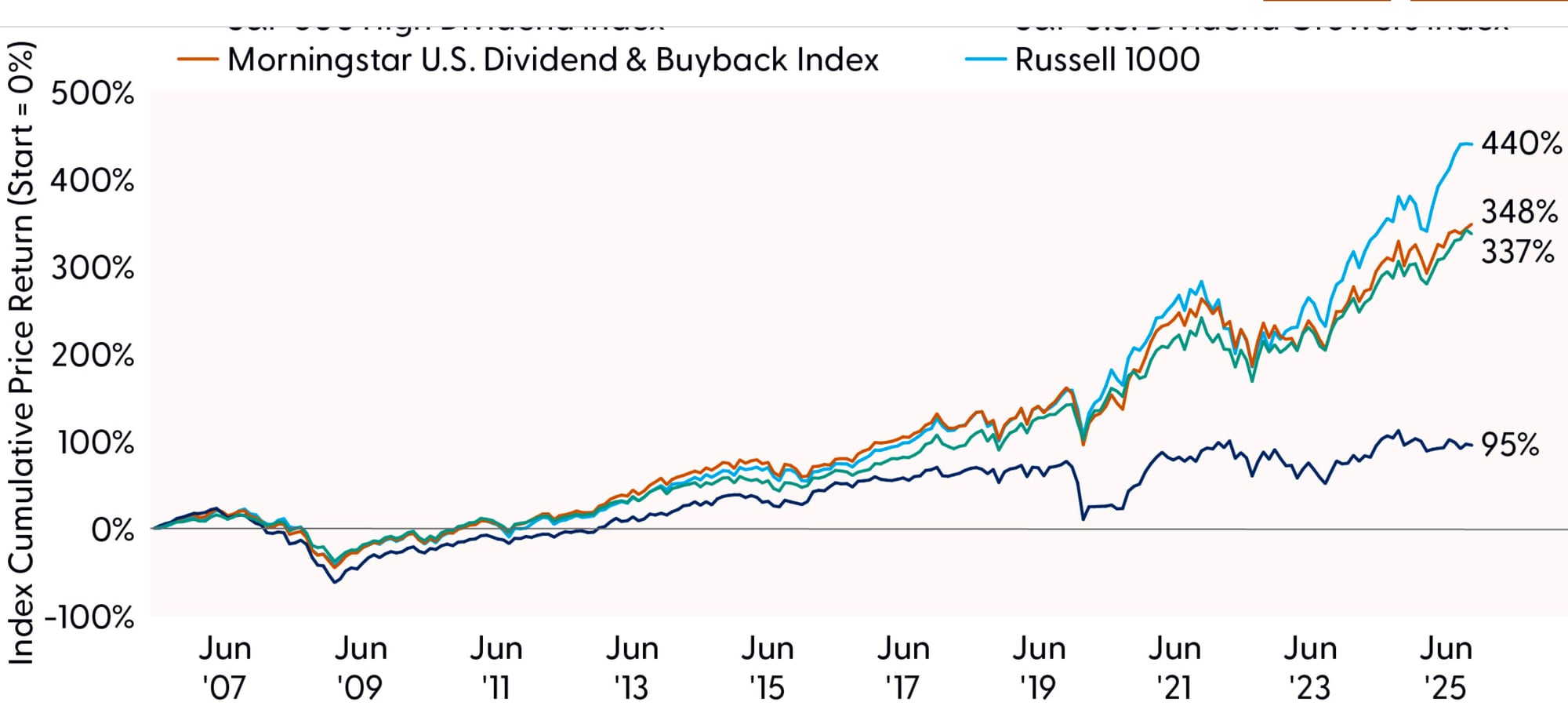

There is empirical evidence, by way of established third-party equity indexes, that enhanced equity income strategies such as these have generated compelling returns relative to simple high dividend yield strategies. Indexes that follow a shareholder yield index, such as the Morningstar U.S. Dividend and Buyback Index and those that follow a dividend growth index, like the S&P U.S. Dividend Growers Index have generated higher total return (inclusive of reinvested dividends) as well as higher capital appreciation (measured by cumulative price returns) than a basic high dividend yield index like the S&P 500 High Dividend Index.

Historical Total Returns Are Compelling for Enhanced Dividend Strategies

Price-Based Returns Have Driven Dispersion Among Equity Income Strategies

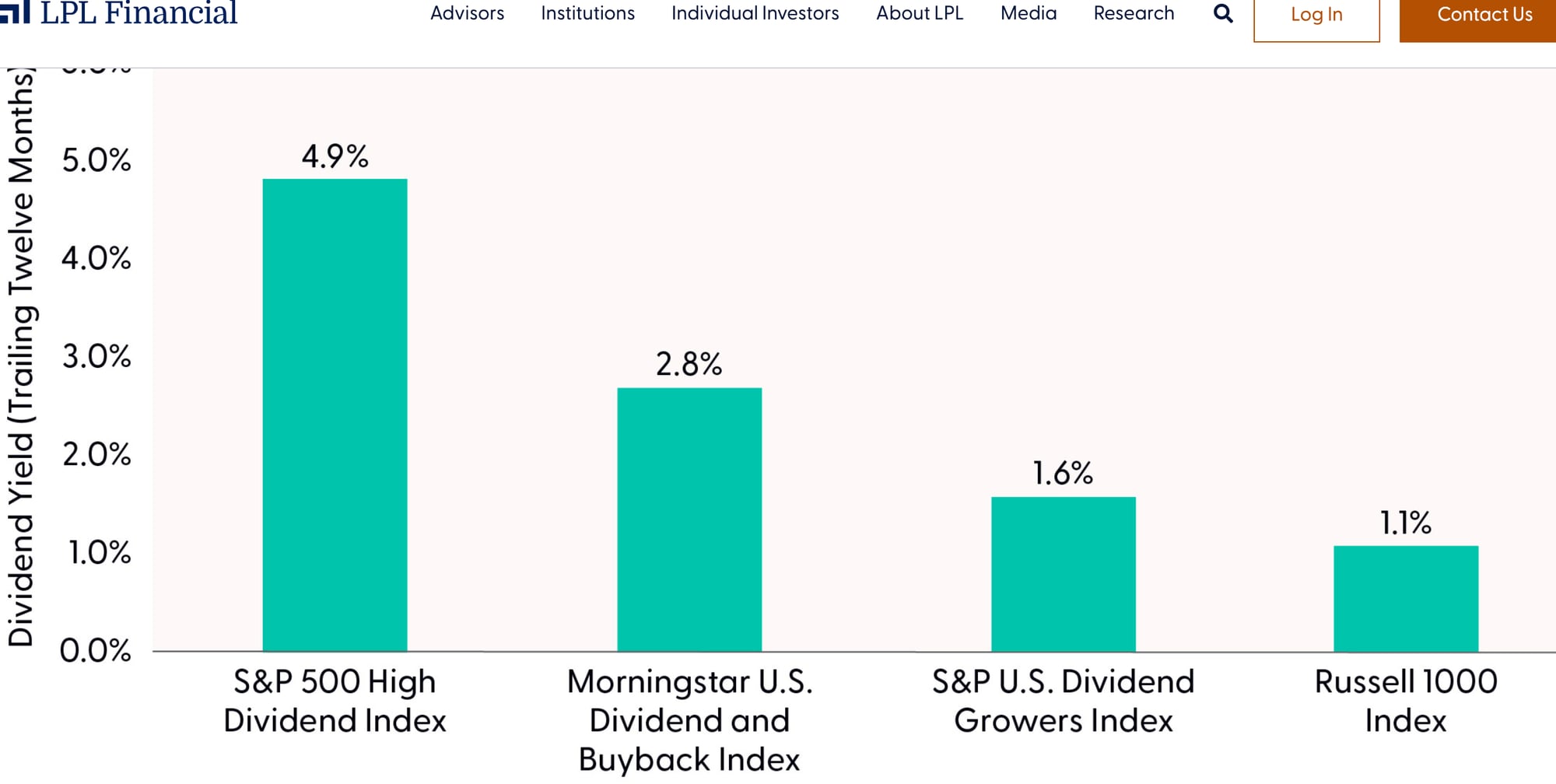

Capital Appreciation Tradeoff: High-Dividend Strategies Provide Higher Current Income

Current Technical Setup: Dividend Stocks Continue to Climb

Conclusion

Our analysis of equity income strategies suggests there is value in a multi‑faceted approach that looks beyond dividend yields. The insights gleaned from this analysis apply to building rules-based screens or systematic “quant” strategies as well as supporting discretionary “quanta‑mental” investment processes, where factor insights inform, but do not replace fundamental judgment. Technical analysis suggests recent outperformance of the basic high dividend strategy may be fleeting and that both of the enhanced equity income strategies show better relative strength.

Looking ahead, the historical results make clear that simple dividend screens may not be adequate for today’s market environment. As capital allocation practices evolve and corporate balance sheets continue to diverge in quality, the opportunity set for equity income investors will increasingly support looking to approaches that go beyond headline dividend yields. A continued shift toward strategies that balance income with capital appreciation (dividend growth), total shareholder return (shareholder yield), and balance‑sheet strength (quality integration) will be essential for generating more resilient outcomes over time.

Adam Turnquist, Chief Technical Strategist, LPL Financial

Tom Shipp, Head of Equity Research, LPL Financial

You may also be interested in:

- LPL Research’s 2026 Strategic Asset Allocation — February 23, 2026

- From Bubble Fears to Disruption Risk: The New AI Market Narrative — February 17, 2026

- Five Reasons the Run in Emerging Markets Could Continue — February 9, 2026

Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-0006767-0226 | For Public Use | Tracking #1071896 (Exp. 03/2027)